Sorry for the infrequent posting of late.

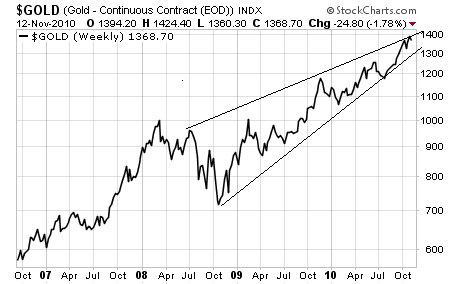

The USD seems to be trying to stabilise, even as gold prices cool off after striking new highs.

Here is a fantastic article that addresses the topic of Banana Republics!

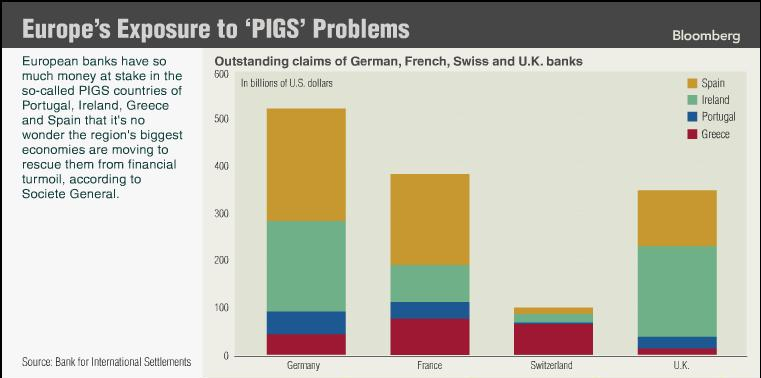

Currency wars / manipulation continue and as bailout packages are announced, many are still asking questions as to who the final beneficiaries of these handouts will be ??

Here's an excerpt from the NY Times article of Nicholas Kristof -

The richest 1 percent of Americans now take home almost 24 percent of income, up from almost 9 percent in 1976. As Timothy Noah of Slate noted in an excellent series on inequality, the United States now arguably has a more unequal distribution of wealth than traditional banana republics like Nicaragua, Venezuela and Guyana.

C.E.O.’s of the largest American companies earned an average of 42 times as much as the average worker in 1980, but 531 times as much in 2001. Perhaps the most astounding statistic is this: From 1980 to 2005, more than four-fifths of the total increase in American incomes went to the richest 1 percent.

That’s the backdrop for one of the first big postelection fights in Washington — how far to extend the Bush tax cuts to the most affluent 2 percent of Americans. Both parties agree on extending tax cuts on the first $250,000 of incomes, even for billionaires. Republicans would also cut taxes above that.

The richest 0.1 percent of taxpayers would get a tax cut of $61,000 from President Obama. They would get $370,000 from Republicans, according to the nonpartisan Tax Policy Center. And that provides only a modest economic stimulus, because the rich are less likely to spend their tax savings.

At a time of 9.6 percent unemployment, wouldn’t it make more sense to finance a jobs program? For example, the money could be used to avoid laying off teachers and undermining American schools.

Likewise, an obvious priority in the worst economic downturn in 70 years should be to extend unemployment insurance benefits, some of which will be curtailed soon unless Congress renews them. Or there’s the Trade Adjustment Assistance program, which helps train and support workers who have lost their jobs because of foreign trade. It will no longer apply to service workers after Jan. 1, unless Congress intervenes.

So we face a choice. Is our economic priority the jobless, or is it zillionaires?