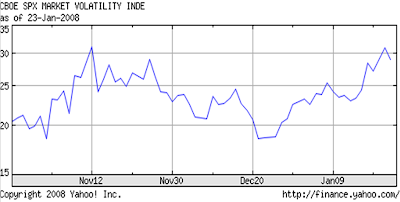

THE LAST 3 MONTHS

EUROPEAN MARKETS ALSO CONTINUE TO STRUGGLE

THE LAST 5 DAYS

CAC 40 : ^FCHI

FTSE 100 : ^FTSE

DAX : ^GDAXI

THE LAST 3 MONTHS

Philadelphia FED DATA: The Diffusion Index of Current Activity.

Manufacturing in the Philadelphia region slowed significantly. The Index fell to a negative 20.9 in January, its lowest level since October 2001. Taken from the Philadelphia FED's Survey, it is considered to be the broadest measure of manufacturing conditions. http://www.philadelphiafed.org/

BOND INSURERS IN REAL TROUBLE

Bond insurers risk losing their AAA rating, as they struggle to raise fresh capital.

Here's what happened>>>

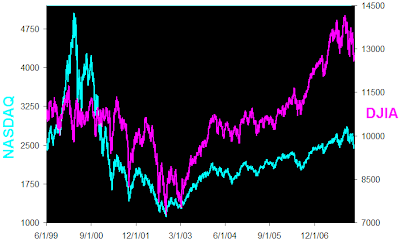

Fed Rates hit a 45 year low of 1% in 2003.  The US Stock Market rallied, as the Goldilocks economy(moderate economic growth : not too hot or cold & low inflation, ) continued on its way.

The US Stock Market rallied, as the Goldilocks economy(moderate economic growth : not too hot or cold & low inflation, ) continued on its way.

Through 2004 & 2005 the US Dollar staged a comeback as interest rates started to rise, only to resume its downtrend in 2006 as the US Housing market started to crumble.

Through 2004 & 2005 the US Dollar staged a comeback as interest rates started to rise, only to resume its downtrend in 2006 as the US Housing market started to crumble.

High debt levels, falling US home prices, and rising interest rates have resulted in a mega catastrophe. US Consumer Confidence is low and as the economy continues to slow, the US consumer will cut back on spending. Huge cash infusions by Central Banks and bailouts by Arab and Asian investors have been unavoidable as leading investment banks are struggling to meet regulatory capital adequacy requirements. The mess in the derivative markets continues, with concerns over losses in Credit-default swaps, and many mortgage backed derivative securities now being seen as toxic WMDs.

Uncontrolled credit expansion encourages reckless consumption and excessive leverage. When the prices of leveraged & overvalued assets start to unwind, the consequences are disastrous.

So are we heading for a "Stagflationary" Bear Market in the US?

Slow economic growth, Inflation and relatively high unemployment = Stagflation

Gold has always done well in such periods, when Central Banks are unable to raise rates to combat inflation due to slowing growth.

Meanwhile, economies such as India and China are consuming increasing quantities of oil, raw materials and food grains as the standard of living across the region continues to rise. Due to their low cost advantage, Asian economies are emerging as manufacturing centres of the world, as production activities continue to shift to developing economies.

Historically, the Gold Oil ratio has support between 8 and 10 barrels per ounce of gold, & spikes over 20 are shortlived.

Is the gold oil ratio going to rebound?

1) oil falls and gold rises

2) gold rises faster than oil

3) oil falls faster than gold

With all the momentum in gold prices recently; fueled by a rising unemployment rate, an increased likelyhood of a recession in the US and a falling USD, gold prices could rise still further, even though gold currently looks overbought.

The possibility of a large FED rate cut is adding to the strength in gold.

Fresh buying can be avoided, waiting for a pull back.

Oil prices are facing a psychological resistance at the $100 mark. Geopolitical concerns, supply disruptions and a falling usd are fuelling high oil prices. A break past $ 100 could propel prices still higher, while a recession in the US will be oil negative.

RICE

RICE